Speech: Jürgen Stark: The global financial crisis and the role of central banking

![]() Autor: Bancherul.ro

Autor: Bancherul.ro

2011-04-13 11:17

The global financial crisis and the role of central banking

Speech by Jürgen Stark, Member of the Executive Board of the ECB,

Institute of Regulation & Risk, North Asia,

Hong Kong, 12 April 2011

It is a pleasure for me to address this distinguished audience. In my remarks today, I would like to share some thoughts with you on how the global financial crisis could shape central banking in the future.

Crises are often associated with deep-seated changes in both the mandates and functions of central banks – this is a well-established regularity in contemporary economic history. For example, central bank inaction was widely held responsible for worsening the economic downturn during the Great Depression of the 1930s. The result was that monetary policy was placed under the control of fiscal authorities for nearly two decades afterwards.

The Great Inflation of the 1970s had the opposite effect. The failure of weak monetary regimes to reign in high inflation led to the establishment, in the early 1980s, of monetary policy frameworks solidly anchored by price stability mandates, and safeguarded by independent and autonomous central bankers.

Will this crisis – which is still ongoing – have any implications for the tasks of central banks in the future?

To shed light on this question, I will, first of all, look back on the salient features of the monetary policy paradigm prevailing before the crisis. Then I will review how central banks responded in practice to the crisis, focusing on the ECB’s policy actions in this regard. And finally, I will discuss whether certain aspects of the pre-crisis monetary policy paradigm need to be reassessed on the basis of the recent experience, and outline the likely challenges for central banks that lie ahead.

***

1. The monetary policy paradigm before the crisis

We do not know yet to what extent the pre-crisis consensus macroeconomic framework has been de-constructed by the crisis. But we do know that the ‘hubris’ of the intellectual paradigm on which that framework was erected has completely vanished.

Some aspects of the framework, in my view, will undoubtedly survive the crisis. One is the great and increasingly shared emphasis on central bank independence. Another is the centrality of price stability for monetary policy. These were the twin foundations of the dominant monetary policy paradigm before the crisis, and the crisis has not challenged or discredited either of them. I will return to the issue of price stability towards the end of my remarks.

Beyond these considerations, other aspects of the international consensus framework merit some careful re-evaluation. In particular, I will take this opportunity to share my thoughts on two salient features of the monetary policy paradigm as described in a number of pre-crisis studies [1].

One was complacency. The ‘great moderation’ of the 1990s appeared to have inflation permanently under control and conveyed the impression that the monetary policy battles of yesteryear had been won once and for all. This sense of security was highly consequential. Some observers thought that monetary policy had a greater freedom to turn to other purposes, notably short-term demand management.

Policy practitioners of this view referred to this as ‘fine-tuning’ [2]. The theoretical counterpart to this was a form of ‘flexible inflation targeting’ with an added emphasis on output stabilisation beyond inflation stabilisation.

Simplifying, one can express the inflation targeting policy advice in two main precepts. First, look at inflation and output gap forecasts as summary statistics of the state of the economy. Second, fine-tune the policy instrument so that inflation forecasts – whatever the nature of the shocks that might have caused them – are stabilised, and output volatility is minimised, at a pre-set horizon through a given interest rate path.

It is easy to conceive of economic conditions in which these prescriptions induce destabilising action on the side of monetary policy. Indeed, limiting the information set to inflation and output gap forecasts can be highly misleading. One reason for this has been known for a long time: output gaps are ill-defined objects and are subject to a great deal of measurement error. An imperfectly understood concept which – in addition – is statistically very imprecisely measured is not a reliable indicator for guiding policy.

Paradoxically, with its focus on the output gap, pre-crisis consensus macroeconomics ran full circle back to the intellectual climate of the 1970s, the same climate that had favoured the Great Inflation. The major policy failures of the 1970s were largely due to policymakers’ exaggerated real-time measures of economic slack.

The second distinctive feature of the pre-crisis monetary policy paradigm stemmed from a complete under-appreciation of the role of money and credit indicators in the conduct of monetary policy. Liquidity and money lie at the core of the ECB’s second pillar. But they were at best ignored, at worst ‘derided’, as redundant and unnecessary complications by mainstream modellers before 2007.

The crisis has shown that liquidity and various definitions of money are critical links in the transmission mechanism. Far from showing a lack of theoretical foundations in the ECB’s strategy, the crisis has exposed the incompleteness of the transmission mechanism in the reference model.

But disregard for monetary and financial phenomena had another implication. It found a clear counterpart and theoretical underpinning in the risk management approach to asset price trends. The consensus view in pre-crisis times was that the best thing that central banks could do was to ‘clean-up’ following the bursting of a bubble by loosening the monetary policy stance.

I do not need to underline how this approach can turn into a formidable multiplier of market turbulence. The expectation that the central bank will aggressively protect the markets from ‘tail events’ in bad times can encourage – and did encourage, in my view – markets’ tendency to opt for risky strategies, over-exposures and exuberance.

In summary, there was an inherent contradiction in some of the salient features of the pre-crisis monetary policy paradigm. On the one hand, central bank policy ‘activism’ was seen as justified in order to help with short-term output stabilisation purposes. Yet activism did not apply to financial risks except in an entirely ex post fashion: proponents of policy ‘activism’ saw no merit in a central bank’s ex ante intervention to stem asset price developments, arguing that the policy interest rate was too blunt a tool to contain potential bubbles.

2. Central bank response to the crisis and ‘the new normal’

The central bank response to the crisis, by any metric, has been unprecedented. When tensions in the interbank market emerged in the euro area and elsewhere in August 2007, the ECB reacted swiftly by providing de facto unlimited overnight liquidity to limit euro area banks’ liquidity risk.

As the tensions morphed into a large-scale crisis of confidence in October 2008, the ECB responded with a mix of standard and non-standard monetary policy actions to foster financing conditions and enhance its credit support to the euro area economy, all with a view to maintaining price stability.

The standard measures essentially entailed a steep reduction of the main refinancing rate to a historical low of 1% over a seven-month period (October 2008 – May 2009). This was done in reaction to the weak economic environment and the associated change in the inflation outlook.

The non-standard measures included granting banks unlimited access to central bank liquidity against an extended range of collateral with the possibility for banks to borrow liquidity at a broader spectrum of maturities, of up to 12 months. The ECB also intervened directly in some market segments that were dysfunctional, namely the covered bonds market. This was deemed important for the long-term financing of banks.

In May 2010 the financial crisis took a different direction; markets started to question the sustainability of public finances in parts of the euro area. In response, the ECB intervened in some debt securities markets, in order to prevent large and important segments of the securitised credit market seizing up and obstructing monetary policy transmission. These interventions have been limited in size, and their impact on liquidity creation has been fully sterilised.

Overall, the non-standard measures have been adopted with a view to ensuring the transmission of low policy rates to the euro area economy. They have been tailored to the specific financial structure of the euro area economy, whose financing to a large extent relies on banks. These measures are fully in line with the ECB’s price stability objective.

In this regard, the approach chosen by the ECB and the Eurosystem differs from that of other major central banks which embarked on large-scale unconventional measures to replace, rather than complement, standard actions, after those standard actions – changes in the policy interest rate – had reached their lower limit. In this respect, the ECB’s non-standard response does not qualify as a form of quantitative easing or credit easing.

Non-standard monetary policy measures are an extraordinary response to exceptional circumstances. They are, by construction, temporary in nature. Looking ahead, a return to a more normal liquidity management and to a more moderate scale of central bank intermediation is warranted to avoid distortions in financial incentives with longer-term adverse consequences for the economy. The ECB started in fact to phase out a number of non-standard measures back in late 2009.

The maintenance of price stability over the medium term guides all monetary policy decisions. In this respect, the macroeconomic and financial landscape has fundamentally changed and the monetary policy stance has become more accommodative than at the peak of the crisis.

As with the phasing-in of non-standard measures, there are no pre-defined steps between phasing them out and exiting from very low policy interest rates. Non-standard measures can in fact co-exist with any interest rate level. The ECB will adjust its policy interest rates and its provision of liquidity at a pace and to a degree commensurate with the evolution of risks to price stability and as appropriate to maintain an orderly and functional monetary policy transmission.

A number of key principles, which served the ECB well both before and during the crisis, will continue to underlie the post-crisis ‘steady state’ design of the ECB’s operational framework. These principles are: operational efficiency, a strong market orientation, simplicity and transparency, and equal treatment of our counterparties.

[In line with these principles, the ECB equipped itself with a broad operational framework from the outset, including the eligibility of a large number of counterparties and a wide set of collateral in refinancing operations. At the same time, the post-crisis operational framework also needs to be designed in a way that contributes to shaping a healthy banking sector, even if proper incentives should essentially come from sound regulation and supervision].

3. The future of central banking and main challenges ahead

What are the desirable features of a post-crisis ‘steady state’ monetary policy framework? On this subject, I would like to make a number of points.

As I mentioned already, the ‘core’ elements of the monetary policy paradigm have emerged from the crisis unscathed. I firmly believe that price stability is the best contribution that monetary authorities can make to overall economic welfare. Price stability should remain the primary task and the key ‘deliverable’ for central banks in the period ahead.

If anything, the crisis has reaffirmed the importance of having a clearly defined objective for price stability, not least by contributing to the anchoring of expectations during periods of turbulence, when otherwise the private sector would become disoriented.

Central bank independence under a specific mandate together with transparent communication policies will continue to be instrumental in the pursuit of price stability by monetary authorities.

Other aspects of the pre-crisis monetary policy paradigm need to be carefully re-examined.

The crisis should mark a clean break with short-termism and ‘fine-tuning’ demand management by monetary authorities. An insufficient medium-term orientation and a systematic asymmetry in responding to shocks – with downside risks to the economy always receiving a greater weight in central bankers’ ‘policy preferences’ than upside risks to price stability – all of this contributed to the build-up of financial imbalances in some advanced economies.

The sudden unwinding of these imbalances set in motion the chain of events which we now call ‘the crisis’. Greater medium-term orientation in monetary policy frameworks would have made the events which followed less severe.

Monetary data are critical as indicators of risks that are slow to appear elsewhere, for example, in inflation forecasts or in measures of output gaps. Monetary analysis at the ECB has consistently sent early signals that risk was broadly under-priced, when inflation was quiescent and measures of slack were moderate.

Incorporating monetary phenomena in the policy framework inspires a sort of ‘leaning-against-the wind’ stance which can help smooth financial cycles and stabilise the economy in the medium term. Coupled with the inescapable fact that inflation is a monetary phenomenon in the long term, this is a powerful reason to redress the under-appreciation of monetary and credit variables in policy frameworks characteristic of the policy paradigm in the run-up to the crisis.

The crisis has shown that central banks have powerful instruments at their disposal to effectively respond to extraordinary situations without compromising their ultimate objective.

However, this does not mean that monetary policy is liable to be subordinated to financial stability concerns. The ECB is well aware of the possibility of monetary policy being ‘contaminated’ by financial stability considerations. Monetary policy – even in crises and, I would say, particularly in crises – is about lending temporarily to solvent institutions. Lending to institutions which have long-lasting, structural funding and equity problems is the responsibility of the fiscal authority.

The limits to what monetary policy could and should credibly do are both conceptual and practical: monetary authorities cannot be expected to solve issues which lie well outside their official remit.

There are two sides to this simple truth, one concerning financial regulation and one broad economic management.

On the financial side, the ECB has a major stake in the quest for financial stability – but the authority lies elsewhere. Basel III is a very important step in the right direction, as it should provide for higher minimum capital requirements and better risk capture by financial institutions. But in addition to the progressive roll-out of this framework and its incorporation into domestic law, the treatment of systemically important financial institutions and risk capture by the shadow banking sector remains to be addressed. It is important to achieve a level playing field in these areas and that bodies such as the Financial Stability Board continue to work to accomplish such an objective. Market regulation on, for example, over-the-counter instruments, alternative investment vehicles and ratings agencies is also an issue in this context.

On the economic side, at the European level, the key challenge is to bring the ‘economic’ part of E-M-U up to speed with the ‘monetary’ part. The crisis has shown that the overall system of economic governance was in need of fundamental reform.

Pro-cyclicality was not confined to monetary policy before the crisis. Actually, too many economies in the euro area entered the acute phase of the financial crisis with insufficient room for manoeuvre, because they had not behaved counter-cyclically before. Policy hyper-activism was another feature of fiscal policy management before the crisis, and the crisis exposed it in a spectacular way.

European leaders have responded by taking a number of important steps to remedy the situation, including measures to improve economic policy coordination in budgetary decisions, such as the so-called ‘European Semester’. A new macroeconomic surveillance framework will be established in order to check deviant behaviour at an early stage. The Stability and Growth Pact (SGP) will also be reformed to enhance the surveillance of fiscal policies and apply enforcement measures at an early stage.

In addition to these EU-wide proposals at the legislative level, a separate pact (the Euro Plus Pact) has been drawn up by the euro area countries and several other EU Member States in order to redress competitiveness differences, thereby further strengthening the economic pillar of EMU.

These measures, once fully operational, would certainly improve the economic governance of the euro area. But strict implementation is key, so that the concept of ‘effective peer review’ in the Union regains credibility among market participants and the public.

The ECB regards the reforms made to the macroeconomic and budgetary surveillance framework as not ambitious enough: they appear to leave room for discretion by Member States to escape sanctions in the event of non-compliance. More automaticity in this regard would be preferable.

4. Conclusion

In conclusion, I believe that the crisis has exposed a couple of shortcomings in the monetary policy paradigm: policy frameworks are insufficiently medium term-oriented, and the role of monetary variables in this context is underappreciated.

But the core elements of the paradigm, including central bank independence and policies decisively oriented towards the maintenance of price stability, remain pertinent for the period ahead.

Central banks have taken unprecedented steps to safeguard this overriding objective during the crisis. Looking ahead, it is up to other key stakeholders in the global financial and economic system to live up to their collective responsibilities and mandates in order to avoid any repetition of past mistakes.

[1] See, for example, Goodfriend, M. (2007) How the World Achieved Consensus on Monetary Policy, Journal of Economic Perspectives 21 (4), pp. 47-68; and Woodford, M. (2008), Convergence in Macroeconomics: Elements of the New Synthesis, paper presented in the session “Convergence in Macroeconomics?”, annual meeting of the American Economic Association, January 2008.

[2] See Blinder, A.S. and Reis, R. (2005), Economic Performance in the Greenspan Era: The Evolution of Events and Ideas, paper presented at the Federal Reserve Bank of Kansas City Symposium on ‘Rethinking Stabilization Policy’, Jackson Hole, Wyoming.

See, for example, Goodfriend, M. (2007) How the World Achieved Consensus on Monetary Policy, Journal of Economic Perspectives 21 (4), pp. 47-68; and Woodford, M. (2008), Convergence in Macroeconomics: Elements of the New Synthesis, paper presented in the session “Convergence in Macroeconomics?”, annual meeting of the American Economic Association, January 2008.

See Blinder, A.S. and Reis, R. (2005), Economic Performance in the Greenspan Era: The Evolution of Events and Ideas, paper presented at the Federal Reserve Bank of Kansas City Symposium on ‘Rethinking Stabilization Policy’, Jackson Hole, Wyoming.

European Central Bank

Directorate Communications

Press and Information Division

Comentarii

Adauga un comentariu

Adauga un comentariu folosind contul de Facebook

Alte stiri din categoria: Noutati BCE

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%, in cadrul unei conferinte de presa sustinute de Christine Lagarde, președinta BCE, si Luis de Guindos, vicepreședintele BCE. Iata textul publicat de BCE: DECLARAȚIE DE POLITICĂ MONETARĂ detalii

BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

Banca Centrala Europeana (BCE) a majorat dobanda de referinta pentru tarile din zona euro cu 0,75 puncte, la 2% pe an, din cauza cresterii substantiale a inflatiei, ajunsa la aproape 10% in septembrie, cu mult peste tinta BCE, de doar 2%. In aceste conditii, BCE a anuntat ca va continua sa majoreze dobanda de politica monetara. De asemenea, BCE a luat masuri pentru a reduce nivelul imprumuturilor acordate bancilor in perioada pandemiei coronavirusului, prin majorarea dobanzii aferente acestor facilitati, denumite operațiuni țintite de refinanțare pe termen mai lung (OTRTL). Comunicatul BCE Consiliul guvernatorilor a decis astăzi să majoreze cu 75 puncte de bază cele trei rate ale dobânzilor detalii

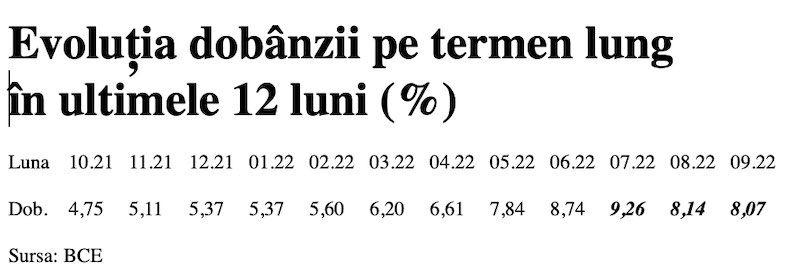

Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Dobânda pe termen lung pentru România a scăzut în septembrie 2022 la valoarea medie de 8,07%, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator, cu referința la un termen de 10 ani (10Y), a continuat astfel tendința detalii

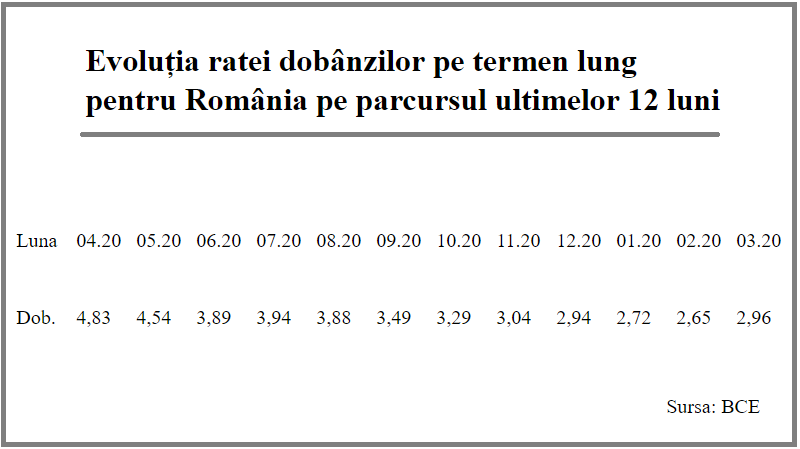

Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Rata dobânzii pe termen lung pentru România a crescut la 2,96% în luna martie 2021, de la 2,65% în luna precedentă, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator critic pentru plățile la datoria externă scăzuse anterior timp de șapte luni detalii

- BCE recomanda bancilor sa nu plateasca dividende

- Modul de functionare a relaxarii cantitative (quantitative easing – QE)

- Dobanda la euro nu va creste pana in iunie 2020

- BCE trebuie sa fie consultata inainte de adoptarea de legi care afecteaza bancile nationale

- BCE a publicat avizul privind taxa bancara

- BCE va mentine la 0% dobanda de referinta pentru euro cel putin pana la finalul lui 2019

- ECB: Insights into the digital transformation of the retail payments ecosystem

- ECB introductory statement on Governing Council decisions

- Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

- Deciziile de politica monetara ale BCE

Profil de Bancher

-

Catalin Iancu, Presedinte

OTP Asset Management

Anul 2012 va fi, in primul rand, unul al luptei ... vezi profil

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent, aproape 18 miliarde euro după primele opt luni

- Deficitul contului curent, peste 9 miliarde euro pe primele cinci luni

- Deficitul contului curent, 6,6 miliarde euro după prima treime a anului

- Deficitul contului curent pe T1, aproape 4 miliarde euro

- Deficitul contului curent după primele două luni, mai mare cu 25%

Legislatie

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

- Reguli privind stabilirea ratelor de referinţă ROBID şi ROBOR

Lege plafonare dobanzi credite

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

- Parlamentul dezbate marti legile de plafonare a dobanzilor la credite si a datoriilor cesionate de banci firmelor de recuperare (actualizat)

Anunturi banci

- Cate reclamatii primeste Intesa Sanpaolo Bank si cum le gestioneaza

- Platile instant, posibile la 13 banci

- Aplicatia CEC app va functiona doar pe telefoane cu Android minim 8 sau iOS minim 12

- Bancile comunica automat cu ANAF situatia popririlor

- BRD bate recordul la credite de consum, in ciuda dobanzilor mari, si obtine un profit ridicat

Analize economice

- România, pe locul 16 din 27 de state membre ca pondere a datoriei publice în PIB

- România, tot prima în UE la inflația anuală, dar decalajul s-a redus

- Exporturile lunare în august, la cel mai redus nivel din ultimul an

- Inflația anuală a scăzut la 4,62%

- Comerțul cu amănuntul, +7,3% cumulat pe primele 8 luni

Ministerul Finantelor

- Datoria publică, 51,4% din PIB la mijlocul anului

- Deficit bugetar de 3,6% din PIB după prima jumătate a anului

- Deficit bugetar de 3,4% din PIB după primele cinci luni ale anului

- Deficit bugetar îngrijorător după prima treime a anului

- Deficitul bugetar, -2,06% din PIB pe primul trimestru al anului

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- ANPC pierde un proces cu Intesa si ARB privind modul de calcul al ratelor la credite

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

Stiri economice

- Datoria publică, 52,7% din PIB la finele lunii august 2024

- -5,44% din PIB, deficit bugetar înaintea ultimului trimestru din 2024

- Prețurile industriale - scădere în august dar indicele anual a continuat să crească

- România, pe locul 4 în UE la scăderea prețurilor agricole

- Industria prelucrătoare, evoluție neconvingătoare pe luna iulie 2024

Statistici

- România, pe locul trei în UE la creșterea costului muncii în T2 2024

- Cheltuielile cu pensiile - România, pe locul 19 în UE ca pondere în PIB

- Dobanda din Cehia a crescut cu 7 puncte intr-un singur an

- Care este valoarea salariului minim brut si net pe economie in 2024?

- Cat va fi salariul brut si net in Romania in 2024, 2025, 2026 si 2027, conform prognozei oficiale

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

- Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

- O firma care a facut un schimb valutar gresit s-a inteles cu banca, prin intermediul CSALB

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- Producția industrială, în scădere semnificativă

- Pensia reală, în creștere cu 8,7% pe luna august 2024

- Avansul PIB pe T1 2024, majorat la +0,5%

- Industria prelucrătoare a trecut pe plus în aprilie 2024

- Deficitul comercial, în creștere de la o lună la alta

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate

Ultimele Comentarii

-

Bancnote vechi

Numar de ... detalii

-

Bancnote vechi

Am 3 bancnote vechi:1-1000000lei;1-5000lei;1-100000;mai multe bancnote cu eclipsa de ... detalii

-

Schimbare numar telefon Raiffeisen

Puteti schimba numarul de telefon la Raiffeisen din aplicatia Smart Mobile/Raiffeisen Online, ... detalii

-

Vreau sa schimb nr de telefon

Cum pot schimba nr.de telefon ... detalii

-

Eroare aplicație

Am avut ora și data din setările telefonului date pe manual și nu se deschidea BT Pay, în ... detalii