KPMG: Only three of 27 EU Member States are clearly in favour of a Financial Transactions Tax |

Autor: Bancherul.ro

2012-02-11 11:39 |

|

The European Commission’s proposal for an EU wide tax on financial transactions (FTT) has generated much public and political discussion since it was published on September 28, 2011. President Sarkozy recently announced proposals for a French FTT to be introduced in July 2012, and the issue has been high on the agenda of many EU Member States’ governments, leading to a British veto of recent proposals for fundamental EU reforms addressing the ongoing economic crisis.

The European Commission’s proposal for an EU wide tax on financial transactions (FTT) has generated much public and political discussion since it was published on September 28, 2011. President Sarkozy recently announced proposals for a French FTT to be introduced in July 2012, and the issue has been high on the agenda of many EU Member States’ governments, leading to a British veto of recent proposals for fundamental EU reforms addressing the ongoing economic crisis.

Notwithstanding the potential economic benefits cited by the Commission, there has been significant criticism of the proposal, in particular as to whether it would in fact achieve its economic objectives and as regards its potential negative impact on EU Member States financial sectors and GDP as a whole.

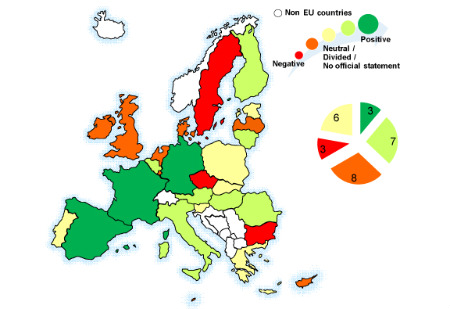

KPMG’s EU Tax Centre, with the help of KPMG member firms and their EU Tax and Financial Services Tax networks, has prepared an informal ´FTT Thermometer´ which displays KPMG member firms’ understanding of the overall position of their respective governments on the FTT proposals.

The review shows that of the 27 Member States, currently only three Member States are clearly in favour, with three clearly against. That leaves another 21 in varying degrees of support, opposition or indecision.

KPMG Comment

“With only three countries clearly in favour, the Commission’s proposal obviously has a long way to go” says Hugh von Bergen, head of KPMG’s Global Financial Services Tax Group. “Some of the Member States which are nominally in favour of the proposal support this subject to an FTT being introduced globally, and the reality is that global introduction is not going to happen, at least not in the foreseeable future. So seen from this angle, the prospects of introduction by the EU seem very uncertain” cautions von Bergen.

“Despite certain Member States’ concerns about relocation and the impact of the proposal on GDP, the Merkel/Sarkozy initiative to push forward the FTT, if necessary on a ‘short-track’ basis with just a few EU Member States, is a strong message to the ‘doubting’ EU Member States” notes Mark Gibbins, Partner and Head of Taxation Services at KPMG in Romania.

“So far little attention has been paid to the question of who gets the revenue from an EU FTT” notes Ionuț Mastacaneanu, Tax Senior Manager at KPMG in Romania. “The Commission sees this as a kind of EU tax that would at least in part support the EU budget. However, even if the principle of an EU FTT was accepted, the question as to how the revenue is shared out – as between the EU and Member States but also between the Member States themselves - is likely to be hotly debated.” Mastacaneanu warns.

LEVEL OF SUPPORT

- Supporting (Green): France, Germany and Spain

- Supporting subject to conditions such as global or EU introduction, and are overall more positive (Lime): Austria, Belgium, Finland, Hungary, Italy, Lithuania and Romania

- Neutral, divided or have not yet expressed an opinion (Light yellow): Estonia, Greece, Poland, Portugal, Slovakia and Slovenia

- Supporting if certain conditions are satisfied, such as global or EU introduction, but are overall less positive (Orange): Cyprus, Denmark, Ireland, Latvia, Luxembourg, Malta, the Netherlands and the UK

- Against (Red): Bulgaria, the Czech Republic and Sweden

Economic background to EU FTT proposal

A tax on financial sector transactions would be an answer to a number of problems largely associated with the financial sector crisis, according to the explanatory memorandum to the European Commission’s draft directive. In particular it would:

- avoid fragmentation of the internal market by coordinating national FTTs

- ensure a fair contribution by the financial sector to the costs of the recent crisis

- ensure a level playing field between the financial sector and other sectors

- remove certain distortions from the financial markets

- provide a source of own revenue for the EU

The European Commission’s original indications were that the directive could generate revenues of around 57 billion euros annually at EU level. Notwithstanding these assumed benefits, the European Commission estimated a negative impact on GDP of between 0.53% and 1.76%. Since then the European Commission is understood to have amended this estimate down to between 0.2% and 0.3%. However, the assumptions underlying these estimates are complex and controversial.

Scope of the FTT proposal

The FTT would be imposed on transactions involving financial instruments carried out by at least one EU based financial institution. The FTT has been designed to cover a wide range of financial transactions, including the purchase and sale of financial instruments such as shares and bonds but also the conclusion of derivatives agreements such as options and futures relating to securities or commodities.

The draft directive provides for a minimum level of FTT of 0.1 percent for financial transactions other than those related to derivatives agreements and 0.01 percent in the case of derivative agreements.

It is only aimed at taxing transactions involving financial institutions and not transactions carried out by ordinary individuals or businesses, such as the conclusion of insurance contracts, nor should it affect most primary market operations. Financial institutions are broadly defined under the draft directive to include traditional financial institutions such as banks and investment entities, but could also cover holding companies, and special purpose vehicles, such as securitization vehicles. Financial institutions can be subject to the FTT even if they act in the name or for the account of another person.

In order for the directive to apply, at least one of the parties to the transaction would need to be established in a Member State. Non EU-based financial institutions may, in certain circumstances, also become subject to the FTT if the transaction involves an EU counter-party. The FTT is chargeable for each financial institution, i.e. the overall rates applicable to a transaction involving two EU counterparties would be 0.2 percent and 0.02 percent for non-derivative and derivative transactions respectively.

Reactions to the FTT proposal

There has been considerable public and political discussion since the proposal was issued. A clear concern that has been raised is the risk that financial sector business will relocate outside the EU to jurisdictions that do not impose such a tax. For this reason a number of governments are understood to only be willing to support the proposal if the FTT is introduced globally.

Notwithstanding this concern, both Germany and France have indicated that, if agreement could not be reached across the whole EU (27 Member States), the tax could be introduced by a smaller group, such as the Eurozone members. Some Member States are understood to take the position that introduction in the EU would be sufficient to address this issue. Questions have also been raised as to whether the FTT is actually the most appropriate instrument to address the economic objectives put forward by the European Commission.

|

|