This paper describes the CNB’s experience implementing an inflation-forecast targeting (IFT) regime, and the building of a system for providing the economic information that policymakers need to implement IFT. The CNB’s experience has been very successful in establishing confidence in monetary policy in the Czech Republic and should provide useful guidance for other central banks that are considering adopting an IFT regime.

We start with an overview of the issues that led the CNB to adopt this regime.

During the 1990s, central bankers came to realize that the better their policies were understood, the more effective they were—a remarkable turnaround within one generation for a profession formerly reputed (not entirely fairly) for secrecy. With respect to numerical variables, the debate at inflation-targeting (IT) central banks has been about what to disclose above and beyond the target for the rate of inflation and the current setting of the policy interest rate instrument—in particular, about what elements of the quarterly macroeconomic forecast of the central bank should be released.

Publishing the forecast for inflation and output has not been controversial, because policymakers had to show the public that they did have a plan for anchoring long-term inflation expectations, and that the plan recognized the potential short-run implications for output. Moreover, Svensson (1997) pointed out that the central bank’s inflation forecast represents an ideal conditional intermediate target, since it takes into account all available information, including the preferences of the policymakers and their view of how the economy works.

The flexible IT regime now in place at many central banks is operationally the same as IFT.

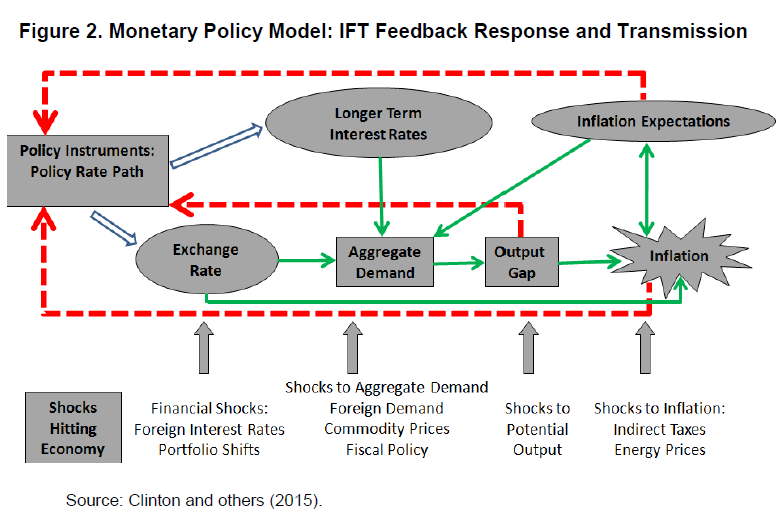

IT logically implies an endogenous interest rate. A model in which the interest rate is exogenous has no nominal anchor—the inflation rate drifts indeterminately following disturbances. Under IT, the nominal anchor for the economy is provided by the expectation that the rate of inflation will converge to the announced long-run objective.

This implies an expectation that in response to any shock, monetary policy will react in such a way as to return inflation to the long-run target. For the policy to be coherent and logically consistent, the interest rate must adjust to the requirements of the target. Many central banks incorporate this principle into their forecasting models and thus produce an endogenous path for the interest rate. However, most of these institutions have, so far, decided not to publish the path, their view being that the policy rate has to be free to respond at any decision meeting to all possible contingencies, and that they do not want to confuse the public by appearing to have a commitment of some kind towards the interest rate.

A leading group of central banks, including the CNB, has gone to full disclosure. This may have been motivated by a desire to increase the transparency of monetary policy, which in itself is surely a good thing, but there have also been solid practical reasons for the move. Any policy interest rate decision by the central bank must involve more than a one-period setting. Changes in the very short-run interest rate controlled by the central bank confined to the short period between policy decision meetings would have negligible macroeconomic effects.

Firms and households borrow and invest at much longer terms. To affect spending, monetary policy has to influence interest rates at these terms, and this requires an influence over market expectations for the future policy interest rate, not just its current level.

Consistent with this, at a given decision, the policymakers must have in mind some path for the future policy rate—albeit a tentative, conditional path, better described by a band than by a single line—when they set the rate for the short period until the next meeting.

In view of the lagged effects of monetary policy, a variety of such paths is possible; and the path chosen by policymakers would reflect their preferences regarding the short-run trade-off between inflation and output. For example, in general, a higher weight on output stability would imply smoother adjustments of the interest rate in response to shocks and a slower return to the long-run inflation target.

Source: IMF Working Paper