Erste Bank: CEE growth drivers intact but innovation is needed to start convergence 2.0 |

Autor: Bancherul.ro

2013-02-20 16:55 |

|

Erste Group press release:

Erste Group press release:

CEE growth drivers intact but innovation is needed to start convergence 2.0

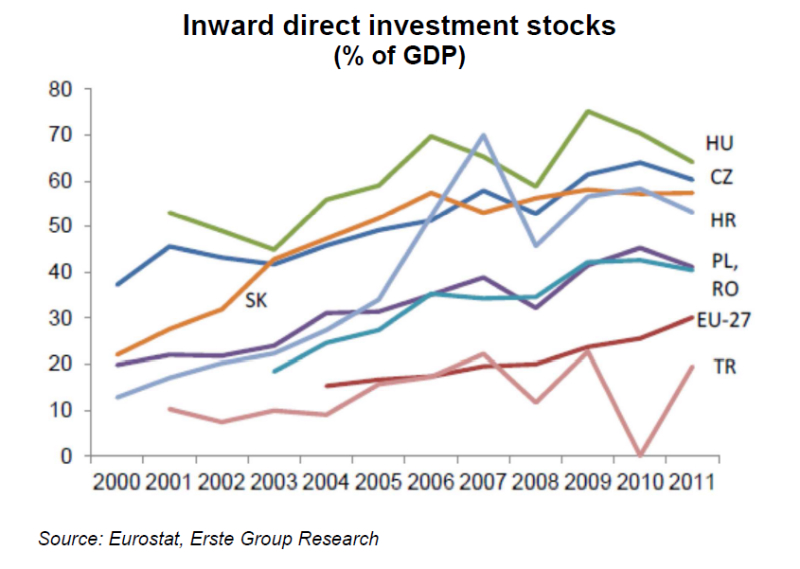

• FDI stock stable at high level, exports still strong but CEE must go beyond the low cost play

• Restarting the convergence machine depends on education and R&D investments to boost innovation

• CEE significantly more industrialized than euro area (30% vs. 19%) but still needs to catch up in terms of competitiveness

• Outlook: next decade is CEE’s window of opportunity to join high-tech league

Since the fall of communism Central and Eastern Europe has become a textbook example of economic convergence through integration into the EU. However, the financial crisis has put a brake on this process.

Erste Group’s special report “Convergence 2.0” published today finds that growth drivers are intact, but over the next decade CEE will have to move from a classical catching up by imitation to a knowledge-based system with more value added and more diversified exports.

“Pure cost competitiveness is not enough when countries are approaching the technological frontier; CEE countries will need to increase productivity of capital and labour by their own means and this makes investments in education and R&D crucial,” explains Birgit Niessner, Chief Analyst of CEE Macro Research at Erste Group.

Among our sample of CEE countries, the Czech Republic, Slovakia and Poland are the frontrunners in terms of competitiveness and knowledge, with Hungary falling behind this group of countries. Romania and Serbia are on their way, but can still exploit more efficiency reserves before becoming innovating economies. Croatia must become more competitive to preserve its relatively high income level, whereas Turkey still has to move towards a knowledge economy.

FDI stock stable at high level, exports still strong but CEE must go beyond the low cost play

CEE countries have used the re-integration of Europe to their own economic benefit and foreign investors have discovered the region as a place to invest in. The countries of the region have thus used their relative cost advantage to modernize their industry with foreign technologies. High stocks of FDI and a high share of exports to GDP are testimony to this and have survived the financial crisis well. The crisis year 2008 constituted a break in the accumulation of the FDI stock, but until 2011, the FDI stock stabilized in all countries.

Hungary’s FDI stock has seen the most negative development: From a peak of 75% of GDP in 2009, it came down by more than 10 percentage points in only two years. Last but not least, another specialty of growth in CEE is excellence in exports. Looking at export’s share of GDP, differences within the CEE region become obvious: starting at already high levels, the CEE-3 countries were able to raise their share of exports in the crisis years. Poland, Croatia and Romania can be found in the middle range, which is partly due to the size of the markets (larger countries tend to export less), but also to non-competitive structures. However, their performance is still superior to the Southern European countries.

So the EU integration has been a success and a factor of paramount importance in the shaping of the economic catch up of the CEE region. The question now is how to reform the integration model of growth. “To use the terminology of the World Economic Forum (WEF) the challenge is to move from efficiency to innovation as drivers of competitiveness. The key to further catching up will be to replace the import of knowledge by innovative and new products generated in CEE countries. Competition, high-quality tertiary education and the availability of venture capital finance will gain in importance,” says Niessner.

The level of tertiary education in CEE is quite diverse, but for most of them it oscillates around 20% of for people aged 30 to 34 and is thus far from the EU target (40%) and the level needed for a labor force engaged in highly innovative sectors.

CEE significantly more industrialized than euro area (30% vs. 19%) but still needs to catch up in terms of competitiveness

CEE economies are dominated by the secondary sector. The share of industry in the overall economic activity oscillates around 30%, whereas the industrial sector in the euro area lies at only 19% of GDP. In terms of overall competitiveness, the CEE countries analyzed in the report hover around a value of 4 on a scale from 1 to 7. This amounts to a rank of 39 for the Czech Republic and a rank of 95 for Serbia, out of 144 countries. Some Western European countries display clearly better ranks, which leaves Erste analysts to conclude that, in terms of a wider concept of competitiveness, CEE still has some way to go. The cost advantage of CEE countries gives them time to do so.

Outlook: next decade is CEE’s window of opportunity to join high-tech league

The question is how much time is left for CEE economies to catch up in terms of productivity, which, together with the long-term development of the labor force, determines the potential output of an economy. The latter is defined as the highest level of GDP that can be sustained over the longer term and offers a view of an economy independent of the economic cycle. During the financial crisis, both actual and potential output growth rates have diminished in most European countries, and the growth rate of potential output even turned negative for Portugal, Greece, Italy and Ireland (on average from 2009 to 2012). “In 2013 and 2014, the growth rates of potential output are forecast to recover to higher levels in CEE countries, with the exception of Hungary. This implies that in the short to medium term, CEE countries will again embark on their path of catching up with the technological frontier. However, as soon as gaps in technology and human capital are closed, productivity growth will slow down and then the above-mentioned deficits in home-grown innovation will become relevant,” concludes the author of the report. Endogenous sources of productivity may also become more important, as the stimulus via FDI and exports may be moderate in the coming years if the crisis carries on.

CEE-4 maintains growth advantage over Western Europe until 2050

The challenge for Central and Eastern Europe in general is to manage the transition from imported productivity gains to endogenous sources of innovation as drivers of growth. Analysts estimate that even in the very long run potential output growth will mainly be driven by productivity gains, as very few European countries can rely on positive demographic dynamics like Turkey. According to OECD forecasts CEE countries will not be able to beat non-OECD countries (e.g. China and India) in terms of growth of potential output. This is due to the already higher level of economic development. However, the Czech Republic, Hungary, Slovakia, Poland and Turkey will continue to outgrow their Western peers by 2050.

(Erste Group’s special report “Convergence 2.0 is in the document attached)

|

|