Jean-Claude Trichet: Current challenges for the euro area

![]() Autor: Bancherul.ro

Autor: Bancherul.ro

2008-10-28 18:36

Current challenges for the euro area

Speech by Jean-Claude Trichet, President of the ECB

�Lunchtime discussions� with the Spanish business community

Madrid, 27 October 2008

Introduction

Ladies and gentlemen,

I would like to thank KPMG and Europa Press for inviting me today to share with you some reflections on the current state of the euro area and its future.

This summer we celebrated the tenth anniversary of the European Central Bank and of the European System of Central Banks, and next January the euro will be ten years old. Since the launch of the euro, the average inflation rate in the euro area has been slightly above 2%. This record compares favourably with the average inflation rate of 3% that was achieved in the member countries in the previous nine years. The ECB has preserved and made available to all euro area countries the stability and credibility that were the privilege of the most successful legacy currencies to be replaced by the euro. Our success in delivering low and stable inflation over the last decade is all the more remarkable when one remembers that, in the early years, the project of a single European currency was received with a degree of scepticism by prominent commentators. These critics have clearly been proven wrong. The euro has rapidly achieved a well-recognised status worldwide as a stable anchor in turbulent times. Far from suppressing growth and entrenching divergences, the euro acts as a vital catalyst for change in the economic landscape of Europe.

Nonetheless, there is no place for complacency. Price stability in the medium term has to be permanently ensured. And the success achieved so far needs to be complemented and consolidated. For this reason, in the remainder of my talk today I would like to discuss the challenges that the ECB, and the euro area as a whole, face as they enter their second decade.

I Price stability: current situation and prospects

Let me first share with you some reflections on the prospects for price stability.

Starting with the current situation, euro area HICP inflation has remained at a high level since last autumn. This spike in euro area HICP inflation had its origins in external forces, in particular the very strong global rise in several commodity prices � notably those of energy and food.

Given the magnitude of these increases in global commodity prices, there has been a sizeable direct pass-through into the food and energy components of inflation. Much of the ongoing inflationary pressure at this stage also derives from the indirect effects on inflation of cost pressures in the production chain. In addition, there is a concern that second-round effects could materialise if consumers or firms attempt to compensate for any loss in purchasing power stemming from the increase in commodity prices by pushing for higher wages or prices.

Available evidence on price and wage-setting behaviour in the euro area suggests some cause for concern in two respects:

First, the indirect impacts on inflation have been strong, given both the scale of the rise in energy and food prices and the fact that these commodities are an extensive input into the production of other goods and services. Strong producer price inflation was not confined to the direct energy and food price components of producer prices. Indirect effects have also been visible at the retail level, most notably in areas with a strong link to energy and food prices, such as the transport and restaurant and caf� components. Ultimately, the extent to which price pressures at early and intermediate stages of production feed through the production chain and up to the retail level crucially depends on the pricing behaviour of firms. An important factor here is the extent of competition in product markets, which obviously serves to reduce the pricing power of individual firms.

Second, labour costs exhibited a clear acceleration in the first half of this year. A pick-up in the growth rate of wages at a time when labour productivity growth is decelerating has resulted in a significant increase in unit labour costs. It is imperative to avoid broad-based second-round effects in wage as well as price-setting. In this context, the ECB has repeatedly expressed its concern about the existence of schemes in which nominal wages are indexed to consumer prices. Such schemes involve the risk of upward shocks in inflation leading to a wage-price spiral, which would be detrimental to employment and competitiveness in the countries concerned.

As for the prospects for inflation, on the basis of current commodity futures prices the annual HICP inflation rate is likely to remain above a level consistent with price stability for some time, moderating gradually during the course of 2009. Taking into account the recent substantial decline in commodity prices, together with the substantial weakening in demand which has emerged lately, upside risks to price stability have diminished. Taking this environment into account and, particularly also the fact that inflation expectations have significantly diminished, the Governing Council has decided to diminish rates by 50 basis points on 8th of October. Assuming that the new information which is progressively becoming available since then and until our next meeting, is likely to indicate a further alleviation of the upside risks to price stability in the medium term and a confirmation of the more solid anchoring of inflation expectations in line with our definition of price stability, I consider possible that the Governing Council would decrease interest rates once again at its next meeting on the 6th of November. It is not a certainty. It is a possibility. If we have decreased rates on the 8th of October it was because upside risks to price stability had diminished and that we were fully confident that the new monetary policy stance would permit us to deliver price stability in the medium term. All our decisions are inspired by this fundamental primary objective: price stability. Any new monetary policy stance that we could decide on at our next regular monetary policy meeting must continue to allow us to tell our 320 million fellow citizens: �you can be confident. We will deliver price stability in line with our definition of less than 2% but close to 2% in the medium term.�

II Potential growth, productivity and structural reforms in Europe

Let me move on to the growth performance of the euro area. Over the short term, annual euro area real GDP growth is expected to slow down. [1] The uncertainty surrounding this outlook is particularly high at the current juncture and, generally, downside risks from the financial market tensions prevail. However, today I would like to look beyond recent developments in economic activity and discuss growth prospects over the medium and long term. I am afraid that prospects for potential output growth over the medium term do not offer a completely reassuring picture. Raising potential output growth remains a challenge for the euro area. [2] Let me elaborate on the three main factors underlying trends in real GDP growth: working-age population growth, labour utilisation and labour productivity. [3]

Working-age population growth remains one important factor explaining disparities in real GDP growth between the euro area and the fastest growing industrial economies. Over the past 20 years, the average contribution to real GDP growth from growth of the working-age population has been approximately 0.8 percentage point higher in the United States than in the euro area. [4] Looking ahead, the euro area faces the prospect of an ageing population, and the labour force could therefore become a strong constraint on the growth potential of the euro area.

As for labour utilisation, over the past ten years, and despite subdued growth in the population of working age, there has been a strong acceleration in the number of total hours worked in the euro area. This stands in contrast to developments in the United States, where a small deceleration has taken place. [5] Much of the euro area acceleration can be explained by enhanced labour utilisation over this period, and the main drivers of this to date can clearly be identified as improvements in participation and employment rates.

However, despite this visible progress, there is room for further improvement with regard to the way in which labour markets work in Europe. First, the employment rate in the euro area remains low by international standards. [6] Second, the unemployment rate is still too high on average in the euro area and especially in certain countries.

As for labour productivity growth, from a longer-term perspective, developments in the euro area have been characterised by a sustained decline. This is in contrast with strong gains in labour productivity in the United States over the past ten years. [7] This acceleration in US labour productivity was triggered by advances in information and communication technology (ICT) during the 1990s. A very favourable regulatory environment, continued investment in research and development (R&D), the ability to redesign management and organisational systems, and the relative ease of reallocating and retraining (as well as shedding) of workers, allowed US firms to benefit from ICT investment and to achieve significant gains in productivity. Developments in the euro area in the last few years suggest that the decline in labour productivity growth may have come to a halt, although at a very low level, and the longer-term effects of the current downturn still have to be assessed. [8] Specific policies aimed at increasing employment, particularly in the unskilled segment of the labour market, have certainly contributed to the slowdown in labour productivity growth, especially in services, which are usually more labour-intensive. However, the developments in labour supply are only part of the story. To a large extent, the slowdown in labour productivity growth can be attributed to a marked slowdown in total factor productivity (TFP) growth, which is generally taken as a measure of technological progress and improvements in the organisation and overall efficiency of production.

These developments described for the euro area have also been seen in Spain, where productivity has been very low over recent years around 0.4% on average over the period 1999-2007. This appears to be related to an increase in employment over the last few years and a production structure more oriented towards labour-intensive sectors, in particular construction and services activities. I am aware that improving productivity in Spain is fully acknowledged as a medium-term challenge by the Spanish authorities, as stated in the country�s National Reform Programme.

To sum up, the prompt and effective implementation of structural reforms � covering the labour and product markets � is essential in order to raise factor productivity and potential output, to create new jobs, to achieve lower prices and higher real incomes, and to increase the resilience and flexibility of the economy. In this context, let me stress that the Lisbon strategy and the peer surveillance of its implementation at the national level have certainly been successful in raising awareness among Member States that structural reforms are decisive, and the institutional environment has indeed significantly improved over the last decade. However, the reform process is far from being complete. The intensity of reform has been uneven across countries. Countries should be encouraged to continue with the reform process irrespective of the phase of the business cycle, and progress towards the Lisbon targets should be the object of constant monitoring and assessment.

I should like to discuss some of the key priorities for reform in three main areas, namely getting more people into work; supporting an innovative environment; and increasing competition.

Getting more people into work. Despite the impressive achievements in job creation, the still relatively high unemployment rates in the euro area, as well as low participation rates in some countries, clearly suggest that there is a need to stimulate not only labour supply but also labour demand. As regards labour demand, it is necessary to reduce labour market rigidities, because they restrict wage differentiation and flexibility and thus tend to discourage the hiring of younger and older workers in particular. Progress towards greater contractual flexibility has remained slow in several euro area countries and employment protection legislation, in particular for permanent contracts, remains fairly rigid. Moreover, in those European countries and regions where competitiveness has declined and/or the unemployment rate remains high, it is important that wage increases do not fully exhaust productivity gains, in order that incentives remain for firms to create additional jobs. As regards labour supply, further reforms in income tax and benefit systems would help to increase incentives to work, in particular for those with weaker ties to the labour market, such as women and older workers.

Supporting an innovative environment. The reforms that I have mentioned need to be complemented by measures supporting innovation through higher investment in R&D and policies geared towards improving human capital. A more entrepreneur-friendly economic environment is also needed, to ensure that new and dynamic firms emerge which can reap the benefits of pursuing creative and innovative ventures.

We know that R&D, as well as human capital, makes valuable contributions to productivity growth. In 2006, R&D investment relative to GDP was only 1.9% in the euro area, compared with 2.7% in the United States. Cooperation between universities, public sector research institutes and industry must also intensify in order to raise the efficiency of public R&D spending. Unfortunately, in several euro area countries investment in human capital is still too low for a �knowledge-intensive� economy. This is a matter of concern since the employability and flexibility of the labour force requires human capital to be continuously adjusted to labour market needs. This investment should start �early�, by enhancing the quality and efficiency of our schools and universities, and should be continued through lifelong training and learning.

Increasing competition. Establishing efficient and well-functioning product and services markets can boost productivity trends by enhancing the incentive to invest and innovate. The long-run dividends offered by competition-enhancing policies cannot be overstated, since �little else other than productivity growth matters in the long run�, as Nobel Prize winner Robert Solow once put it. Moreover, such policies will support employment creation, reduce inflation persistence and keep upward price pressures contained, thereby improving the adjustment capacity of countries. It is undeniable that, over the past two decades, significant progress has already been made under the Single Market Programme. This has already yielded major benefits for European economies. However, the extension and deepening of the Single Market still remains a high priority in order to achieve further financial market integration, effective competition in the energy market and the full implementation of the Services Directive.

III Competitiveness and unit labour cost developments in euro area countries

Having discussed the outlook for inflation and growth � as well as highlighted what are in my view the priority areas in which decisive progress on structural reforms is most urgently needed � I would now like to move on to another key challenge for the euro area countries: improving competitiveness. In this respect, let me elaborate further on developments in unit labour costs, [9] which I briefly mentioned a few minutes ago.

A number of euro area countries have witnessed relatively strong increases in unit labour costs since the beginning of 1999. In particular, in cumulative terms, over the nine-year period from 1999 to 2007, a group of countries witnessed increases in unit labour costs of between 25% and 35%, well above the average euro area cumulative increase of around 14%. In Spain, unit labour costs grew in total by around 26% over this period, compared with less than 2% in the case of Germany and around 4% in the case of Austria.

Differing developments in unit labour costs across the euro area countries from 1999 to 2007 appear to be largely the result of differences in the growth rates of compensation per employee. However, in a few countries, including Spain, the cumulated productivity growth rate over the nine-year period of reference appears to have been outstandingly low, also contributing to above average increases in unit labour costs. Persistent differences in labour cost developments have important implications for the price and cost competitiveness of individual countries and, therefore, an impact on a country�s current account balance through the export channel. Most of the euro area countries that experienced a sizeable loss in price and cost competitiveness over the period 1999-2007 appear to have also seen a worsening in their current account positions. In particular, in Spain, the current account reached a deficit of 10% of GDP.

Three main factors can explain relatively strong cumulated labour cost or price increases in individual countries. First, there are factors that can be linked to the real convergence and economic integration process of a country. In practical terms, however, it is extremely difficult to disentangle the portion of the price and labour cost differentials that may reflect an adjustment to a new equilibrium level. Second, a lack of flexibility in product and labour markets can create, in the case of adverse shocks, persistent relative price and cost increases in the countries affected. The close link between the persistence of wages and inflation may be related to institutional features, such as the presence of some form of automatic price indexation of wages which continues to exist in some countries, including Spain. And third, an economy can suffer a long period of strong demand pressures. These pressures may initially be related to either country-specific demand shocks or an excessive reaction to common shocks, which are then exacerbated by overly optimistic expectations on the part of consumers or firms regarding future income prospects. This situation may be further intensified by an insufficiently tight fiscal stance. Such a situation is likely to lead to an inflationary process and cumulated losses in competitiveness. Moreover, the impact may be seen not only on goods and services prices but also on asset price inflation, notably in housing markets.

What then should be done on the policy side? Let me clarify that country-specific price and labour cost dynamics that result from relatively inefficient institutional arrangements or domestic policies need to be addressed by national policy-makers; as already stressed, structural reforms are key. With respect to labour market policies, governments and social partners must share responsibility for ensuring that sufficient attention is paid to competitiveness and employment in wage determination. In particular, schemes in which nominal wages are indexed to consumer prices should be abolished. Such schemes involve the risk of upward shocks in inflation leading to a wage-price spiral, which would be detrimental to employment and competitiveness in the countries concerned. Furthermore, national authorities can make a substantial contribution to more modest labour cost developments. In particular, the public sector should be a role model in terms of wage-setting and should not contribute to strong overall labour cost growth.

Some countries have already started to witness a correction or unwinding of the imbalances accumulated over the last few years. In this context, the sooner corrective measures are taken by the national authorities, the lower the risks will be of that country experiencing a protracted period of low growth and losses in employment.

Conclusion

Ladies and gentlemen, having covered a number of areas which are at the heart of monetary policy-making in the euro area, let me conclude by summarising some important points. Specifically, I would like to list a number of points which should be kept in mind if we want to preserve and consolidate the remarkable success of the euro and to reinforce the strength and resilience of the euro area economy.

First, in the current uncertain environment it is crucial that the public�s trust in the soundness of fiscal policies is preserved. Therefore, I welcome that the European Council reconfirmed that budget policies must continue to be in line with the provisions of the Stability and Growth Pact. This means that the rules of the Pact should be applied fully, while also reflecting the current exceptional circumstances. Concretely, fiscal policies need to ensure the longer-term sustainability of public finances. For some countries, this implies that there is no leeway for fiscal loosening. By contrast, countries with budgetary room for manoeuvre can let automatic stabilisers operate freely and fully, thus contributing to smoothing the business cycle.

A second building block on which I touched, and through which we will consolidate our success, is structural reforms. As I have said today, the firm implementation of the Lisbon strategy, as refocused and reinforced by the EU Council, is essential in order to augment our growth potential, consolidate sustainable prosperity and job creation, and strengthen the resilience of our economy. This agenda calls for courageous structural reforms. In the current crisis, economic flexibility, including flexibility in prices and wages, is even more important than in more normal times.

Third, as I have explained, it is essential to regularly monitor developments in unit labour costs across the euro area countries. In particular in those countries, such as Spain, where there has been a substantial and long-lasting cumulation of above average increases in labour costs, and therefore losses in competitiveness, it is essential that all social partners understand the importance, in the context of Monetary Union, of moderating cost and price increases. This is crucial in terms of both labour costs and firms� mark-ups. All social partners must understand their shared responsibility in delivering price stability and supporting job creation and a sustainable output growth pattern.

Fourth, we are presently experiencing a period of intense turbulences which correspond to a very significant market correction at a global level, which is extremely demanding for all Institutions whether public or private, for all market participants and for all authorities. The ECB and the Eurosystem together with the other Central Banks have taken a number of decisions as regards the refinancing of commercial banks that were appropriate in view of the exceptional circumstances we had to cope with. Amongst the most recent of these orientations, was the decision to engage in unlimited provision of liquidity for all our refinancing duration, from one week to six months and at a fixed interest rate. Also very significant was the decision to enlarge our collateral framework to facilitate the provision of liquidity to commercial banks in a period of intense stress. I am impressed by the fact that all observers and all our partners have praised our capacity to react rapidly and efficiently to the present exceptional challenges. At the same time, everybody has recognised that the rapidity of our reaction in the domain of commercial banks� refinancing did not hamper our credibility in delivering price stability in the medium term. We made clear since the first days of the turbulence in the beginning of August 2007 that we were making a very clear separation between the monetary policy stance- aiming at delivering price stability over the medium term- and the implementation of that monetary policy stance, taking into account the �policy level� of interest rates.

And fifth, it is precisely because we judged � fully in line with our separation principle � that the alleviation of risks to price stability and the regaining control of inflation expectations were significant and convincing that we decreased rates in October. As I said, it is possible that we would decrease rates again in the occasion of the next meeting of the Governing Council. If we do so � I repeat if - it would be because we would have judged that a further alleviation of inflation risks and a further improvement of inflation expectations fully justify the move.

Let me also say that our last decision to decrease rates was based upon the assumption that our very strong call to price setters and social partners not to engage in second round effects had been not only heard, but understood as being essential in the present circumstances. I would today reinforce my very strong call to all partners concerned.

Thank you very much for your attention.

--------------------------------------------------------------------------------

[1] Euro area GDP growth was 2.7% in 2007, and in the September 2008 ECB staff macroeconomic projections real GDP growth is projected to be between 1.1% and 1.7% in 2008 and between 0.6% and 1.8% in 2009.

[2] Estimates from international institutions project euro area potential output growth to be between 1.8% and 2.0% in 2009 (European Commission 1.8%, OECD 1.9% and IMF 2.0%).

[3] This analysis relies on the commonly used growth accounting framework that links real GDP (Y) to the product of labour productivity (L), labour utilisation (LU) and working-age population (WA), i.e. Y = LP x LU x WA.

[4] Euro area working-age population growth was 0.5% over the period 1987-97 and 0.4% over the period 1998-2007. Over these same two periods US working-age population growth was 1.1% and 1.3% respectively.

[5] Growth in total hours worked accelerated in the euro area from an average of 0.2% per year during the period 1987-97 to 1.0% during the period 1998-2007. Over these same periods growth in total hours worked slowed down in the United States from 1.7% to 0.8%.

[6] The participation rate in the euro area was 71.1% in 2007, while that in the United States was 75.3%. The disparities in participation rates between the euro area and the United States are particularly strong for people aged 55 to 64 (46.3% in the euro area versus 63.8% in the United States) and those aged 16 to 24 (44.7% in the euro area versus 59.4% in the United States).

[7] Measured per hour, average productivity growth in the euro area in the period 1998-2007 was 1.2% and thus clearly lower than the 2.1% recorded in the earlier period 1987-97. US real GDP growth per hour worked has shown a strong increase in recent years, averaging 2.1% over the period 1998-2007, compared with 1.3% over the period 1987-97.

[8] Average annual hourly labour productivity was 1.3% during the period 2005-07, compared with 1.4% during the period 1995-2004. In the United States hourly labour productivity growth declined to 1.2% from 2.1% over the same two periods.

[9] Labour costs per unit of output, which are usually computed as compensation per employee divided by labour productivity.

Comentarii

Adauga un comentariu

Adauga un comentariu folosind contul de Facebook

Alte stiri din categoria: Noutati BCE

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%, in cadrul unei conferinte de presa sustinute de Christine Lagarde, președinta BCE, si Luis de Guindos, vicepreședintele BCE. Iata textul publicat de BCE: DECLARAȚIE DE POLITICĂ MONETARĂ detalii

BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

Banca Centrala Europeana (BCE) a majorat dobanda de referinta pentru tarile din zona euro cu 0,75 puncte, la 2% pe an, din cauza cresterii substantiale a inflatiei, ajunsa la aproape 10% in septembrie, cu mult peste tinta BCE, de doar 2%. In aceste conditii, BCE a anuntat ca va continua sa majoreze dobanda de politica monetara. De asemenea, BCE a luat masuri pentru a reduce nivelul imprumuturilor acordate bancilor in perioada pandemiei coronavirusului, prin majorarea dobanzii aferente acestor facilitati, denumite operațiuni țintite de refinanțare pe termen mai lung (OTRTL). Comunicatul BCE Consiliul guvernatorilor a decis astăzi să majoreze cu 75 puncte de bază cele trei rate ale dobânzilor detalii

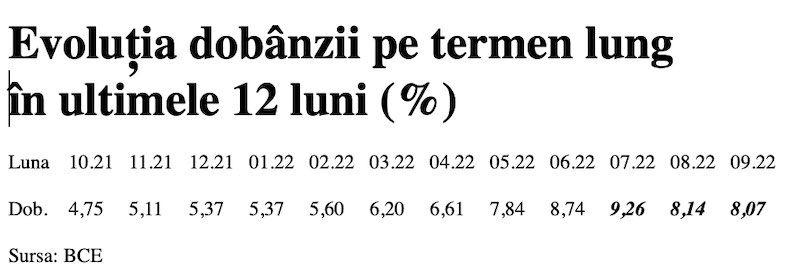

Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Dobânda pe termen lung pentru România a scăzut în septembrie 2022 la valoarea medie de 8,07%, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator, cu referința la un termen de 10 ani (10Y), a continuat astfel tendința detalii

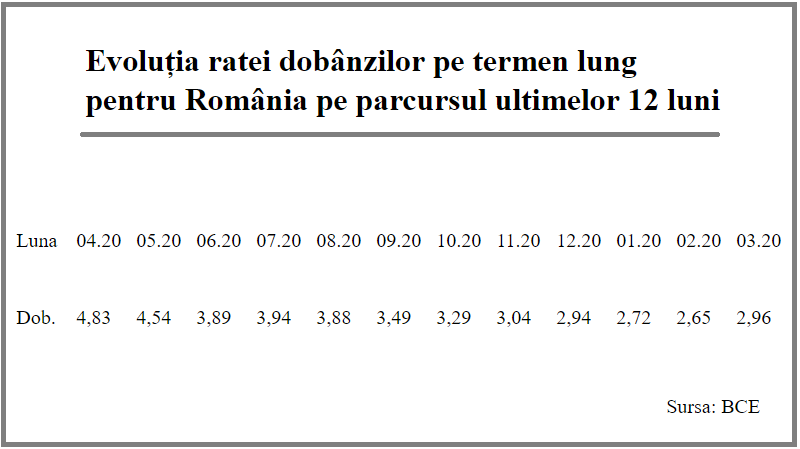

Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Rata dobânzii pe termen lung pentru România a crescut la 2,96% în luna martie 2021, de la 2,65% în luna precedentă, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator critic pentru plățile la datoria externă scăzuse anterior timp de șapte luni detalii

- BCE recomanda bancilor sa nu plateasca dividende

- Modul de functionare a relaxarii cantitative (quantitative easing – QE)

- Dobanda la euro nu va creste pana in iunie 2020

- BCE trebuie sa fie consultata inainte de adoptarea de legi care afecteaza bancile nationale

- BCE a publicat avizul privind taxa bancara

- BCE va mentine la 0% dobanda de referinta pentru euro cel putin pana la finalul lui 2019

- ECB: Insights into the digital transformation of the retail payments ecosystem

- ECB introductory statement on Governing Council decisions

- Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

- Deciziile de politica monetara ale BCE

Profil de Bancher

-

Ana Cernat, Vicepresedinte executiv

Idea Bank

Ana are o experienta de peste 14 ani in domeniul ... vezi profil

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent, aproape 18 miliarde euro după primele opt luni

- Deficitul contului curent, peste 9 miliarde euro pe primele cinci luni

- Deficitul contului curent, 6,6 miliarde euro după prima treime a anului

- Deficitul contului curent pe T1, aproape 4 miliarde euro

- Deficitul contului curent după primele două luni, mai mare cu 25%

Legislatie

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

- Reguli privind stabilirea ratelor de referinţă ROBID şi ROBOR

Lege plafonare dobanzi credite

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

- Parlamentul dezbate marti legile de plafonare a dobanzilor la credite si a datoriilor cesionate de banci firmelor de recuperare (actualizat)

Anunturi banci

- Cate reclamatii primeste Intesa Sanpaolo Bank si cum le gestioneaza

- Platile instant, posibile la 13 banci

- Aplicatia CEC app va functiona doar pe telefoane cu Android minim 8 sau iOS minim 12

- Bancile comunica automat cu ANAF situatia popririlor

- BRD bate recordul la credite de consum, in ciuda dobanzilor mari, si obtine un profit ridicat

Analize economice

- România, pe locul 16 din 27 de state membre ca pondere a datoriei publice în PIB

- România, tot prima în UE la inflația anuală, dar decalajul s-a redus

- Exporturile lunare în august, la cel mai redus nivel din ultimul an

- Inflația anuală a scăzut la 4,62%

- Comerțul cu amănuntul, +7,3% cumulat pe primele 8 luni

Ministerul Finantelor

- Datoria publică, 51,4% din PIB la mijlocul anului

- Deficit bugetar de 3,6% din PIB după prima jumătate a anului

- Deficit bugetar de 3,4% din PIB după primele cinci luni ale anului

- Deficit bugetar îngrijorător după prima treime a anului

- Deficitul bugetar, -2,06% din PIB pe primul trimestru al anului

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- ANPC pierde un proces cu Intesa si ARB privind modul de calcul al ratelor la credite

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

Stiri economice

- Datoria publică, 52,7% din PIB la finele lunii august 2024

- -5,44% din PIB, deficit bugetar înaintea ultimului trimestru din 2024

- Prețurile industriale - scădere în august dar indicele anual a continuat să crească

- România, pe locul 4 în UE la scăderea prețurilor agricole

- Industria prelucrătoare, evoluție neconvingătoare pe luna iulie 2024

Statistici

- România, pe locul trei în UE la creșterea costului muncii în T2 2024

- Cheltuielile cu pensiile - România, pe locul 19 în UE ca pondere în PIB

- Dobanda din Cehia a crescut cu 7 puncte intr-un singur an

- Care este valoarea salariului minim brut si net pe economie in 2024?

- Cat va fi salariul brut si net in Romania in 2024, 2025, 2026 si 2027, conform prognozei oficiale

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

- Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

- O firma care a facut un schimb valutar gresit s-a inteles cu banca, prin intermediul CSALB

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- Producția industrială, în scădere semnificativă

- Pensia reală, în creștere cu 8,7% pe luna august 2024

- Avansul PIB pe T1 2024, majorat la +0,5%

- Industria prelucrătoare a trecut pe plus în aprilie 2024

- Deficitul comercial, în creștere de la o lună la alta

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate

Ultimele Comentarii

-

Bancnote vechi

Numar de ... detalii

-

Bancnote vechi

Am 3 bancnote vechi:1-1000000lei;1-5000lei;1-100000;mai multe bancnote cu eclipsa de ... detalii

-

Schimbare numar telefon Raiffeisen

Puteti schimba numarul de telefon la Raiffeisen din aplicatia Smart Mobile/Raiffeisen Online, ... detalii

-

Vreau sa schimb nr de telefon

Cum pot schimba nr.de telefon ... detalii

-

Eroare aplicație

Am avut ora și data din setările telefonului date pe manual și nu se deschidea BT Pay, în ... detalii